Published: August 15, 2017

Updated: August 22, 2024

Churn happens, and it’s always painful to lose customers. But by digging a little deeper to discover the reasons behind churn, you can improve your product and service while strengthening your customer retention strategy.

If you’re in a business that’s dependant on customer subscriptions, I’m sure you’re very familiar with churn. It’s that pesky little metric that’s a downer at marketing meetings and when you’re trying to forecast growth.

It’s a hole in your bucket when you’re trying to carry water; it’s a pinprick in the balloon you gave your kid. Left unabated, churn can drain you dry and leave you without air.

Customer churn is often viewed as the bane of a company's growth plan, and don’t get me wrong, it sure is. If you’re losing five customers for every five you gain, you’re quickly going nowhere. You need a solid customer retention strategy.

But instead of just saying, ‘Churn sucks!’, and throwing your hands in the air, read on. I’m going to show you the silver lining to customer churn and how it can provide valuable insights into product development, marketing, and customer service.

What is customer churn?

Churn is the percentage at which customers cancel their subscriptions compared to the total amount of new and existing subscriptions you retain. It can be measured by the number of customers you lose per month (customer churn), or by the amount of monthly recurring revenue they represent (MRR churn).

Keeping your eye on both metrics can give you insights into your company's health and make sure you’re retaining customers.

Breaking down customer churn

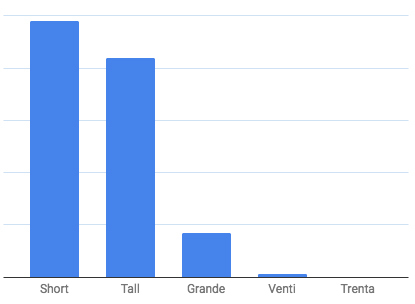

If your company offers different subscription bundles or plans, it’s useful to break churn down into separate buckets for each one. This way you can see which plans are experiencing the highest churn levels and make decisions based on that information.

Say for instance you had 1000 customers and three different subscription plans - small, medium, and large. In one month maybe you had 100 customers churn, but most of them were all on the small plan. This would make your customer churn rate high, but your MRR churn would be low. On the flip side, if you had twenty large customers churn, your customer churn rate would be low, but your MRR rate would be high.

Fighting churn company-wide

Here at Proposify, we’ve noticed that our smaller plans churn at far higher rates than our larger plans. Although the smaller plans represent a bigger portion of our customer base, we decided to focus on increasing subscriptions to our larger plans.

A higher percentage of customers on larger plans would increase our lifetime value (LTV: projected revenue for the lifetime of each customer) as well as significantly lower our MRR churn. Growing our larger subscription base has been a combined effort between the product and marketing departments.

On the product side, we know that people on larger plans write more proposals, so we created features aimed at that market, making it easier for them to manage their accounts and workflows. We added the 'roles and permissions,' and 'teams' features.

The 'roles and permissions' feature allows our account holders to create roles for different types of users on their team, and then restrict their access to certain parts of the app. They have the power to control which proposals certain roles can view or edit, and whether they require approval from the account holder before sending a proposal to a client.

For companies with multiple or regional brands, our 'teams' feature allows each team to have their own branding, pipeline and content, while still being managed under one account.

We received great feedback on these features, and they resulted in two key benefits. Not only did new customers start converting at a higher rate into larger plans, but our existing customer base also expanded up into these plans.

On the marketing side, an effort was made to target small and medium business more through content and social marketing, as they have a greater demand for proposals and a solid sales process.

This interdepartmental effort helped us successfully increase the percentage of larger sized plans to exceed the lower tier plans. This has reduced our MRR churn considerably, making it more stable and less affected when smaller plans churn.

Ask your customer why

It’s important to know which plans are churning and at what rate, but wouldn’t it be more valuable if you knew why customers left? There’s an easy way to find out…ask them!

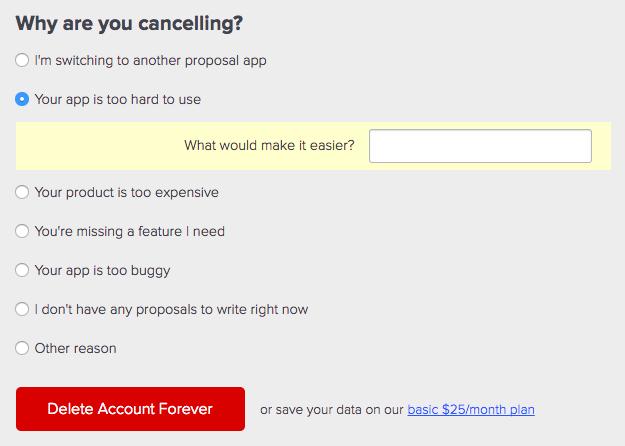

One of the things we do at Proposify that has been invaluable to understanding churn is to ask the customers why they’re cancelling their account when they deactivate. They have to select an option to be able to click on the ‘delete’ button. Once they select a ‘why are you cancelling?’ option, we go a step further and ask them to tell us more.

What’s been really interesting to see is the number of people who honestly answer the question and give us more information about their reasons for cancelling their account.

Before we started asking the follow-up question, we wondered if people just randomly selected an option just to get out the damn door quickly. But after analyzing the results, we could see that people actually told us why and gave more detail. Although some of the feedback is difficult to hear sometimes, it provides us with a deeper understanding of our customer churn.

Each month I get a CSV with all the results, and I pour over them to get a larger sense of why people are leaving. Based on this information, we make product decisions to improve the Proposify experience and ensure that our customers continue to get value from the product.

About a year ago one of the top reasons our customers gave for cancelling their account was that our product was “too buggy,” followed by a mention about the undo feature. We were already aware of the undo problem by listening to our customer support team, but seeing it listed so often in cancellations made us stop in our tracks and set out to fix it.

It did take considerable time for the undo feature to be fixed and shipped; since then we’ve seen a drop in that reason being selected for customer churn. It’s one thing to know why things are happening, but it is an entirely different thing to take charge and make changes.

Voluntary churn vs. involuntary churn

So far I have mostly talked about voluntary churn — people who take action to cancel their account — but there is another kind of churn that can often account for 30 - 40% of your total churn. This silent killer is named ‘involuntary churn.’

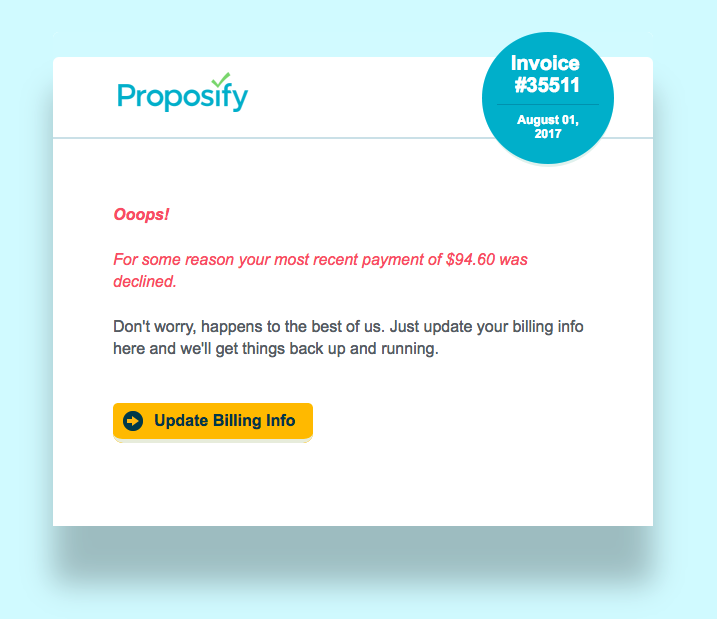

Involuntary churn happens when the recurring payment gets blocked by the bank, or the credit card is expired, or the customer simply doesn’t have enough room on their credit card to cover the subscription fee. While there are many reasons why a payment gets declined, the result is the same: a lost customer. Even though you may send failed payment emails to customers when their payment doesn’t go through, it doesn't mean they’re going to come back.

Digging deeper

Part of our weekly and monthly metrics review is looking at how many transactions are declined. Three months ago we noticed that the number of declines was spiking, so we decided to investigate why.

We poured over the metrics available to us and ended up no further ahead. We spoke with Recurly (our subscription management service) and Stripe (payment gateway) to see if anything had changed on the banking side of things.

We assumed that the banks were being more stringent on which payments were allowed, as we had issues in the past with cross-border payments. Unfortunately, we didn’t learn anything new to help us solve the problem.

After about a week I was pretty frustrated. I could see more and more declined payments and the rate of accounts suspensions going up. 37% of our churn was involuntary when this started, and with the increase we would be at 45% by the end of the month.

I reached out to Recurly again asking what I could do to help this negative trend and ended up on a phone call with their support. We reviewed our dunning process, which is the email campaign that gets sent to a customer if their credit card fails, asking them to change or update their card so they can reactivate their subscription.

We discovered that our dunning process was too short, lasting only seven days, and that the emails contained too much information. We came up with a plan to extend the dunning process to give customers more notice and to simplify the content of the emails.

Once this was in place, we had to sit and wait.

The new extended dunning process meant Recurly made more attempts on the credit cards, which resulted in an even higher failed transaction rate, but it also lowered our involuntary churn rate, which was the real metric we wanted to affect.

Six weeks after the change our involuntary churn rate has dropped to 33%.

Takeaway: Although this story doesn't relate to any epiphany about our customer base, by keeping a watchful eye on our churn and related metrics, we saw a problem before it got out of hand and worked to find a solution.

Understand your customer life cycle, from beginning to end

Having a clearer picture of the breakdown of your churn rates by plan and by churn type can empower you to fix holes before they sink your ship. Although churn is a negative metric, there’s still some value that can come from it.

Since churn is at the end of a customer life cycle, knowing your customer personas and the reasons why they buy or don't buy is a critical aspect of your company’s profitability.

You can apply a lot of the techniques for understanding customer churn to other parts of your customer life cycle to uncover issues before they become problems. The key is to gather data, analyze it, make changes, and measure again.